THE ECONOMY IS SO BAD...

A truckload of Americans was caught sneaking into Mexico

Motel Six won't leave the light on anymore

My neighbor got a pre-declined credit card in the mail

McDonald's is selling the 1/4 ouncer

A picture is now only worth 200 words

Well, maybe it’s not THAT bad, but it’s not good either.

I’m quite fortunate that I live in what the Boardwalk 9:59 Club refers to as “The Bethany Bubble.” The Bubble is a truly wonderful place. We generally have really good weather. In fact, quite often it seems to rain everywhere but the Bubble, much to the dismay of homeowners who want green grass.

Unlike the big cites 100 miles to our north or west, the bubble has very little crime. Sure, there’s the occasional drug bust and some shoplifting, but major crime is really rare. Nearby there was a bank robbery and a murder in 2021 but so far 2022 has been quiet.

The Bubble is also rather affluent with per capita income 70% above the national average and less than 3% of the Bethany Beach population is living below the poverty level. Its unemployment rate is in line with the national rate.

Things are just fine in The Bubble.

But The Bubble isn’t at all representative of the nation as a whole.

We keep hearing our leaders tell us everything is fine, but is it? We hear that unemployment is 3.5%. That sounds good. Hundreds of thousands of jobs are created. That sounds good too.

But is that the whole story? No.

There are massive structural issues with the U.S. economy, many of which the average person hasn’t heard of. Here’s a few….

Unemployment

Every month we hear the rate of unemployment for the prior month. It’s a nice neat number but, as with many things covered on TV news, the rate they announce is only the tip of the iceberg. The Bureau of Labor Statistics (BLS) publishes a boatload of data every month including several rates of unemployment.

The nationally-reported unemployment rate in September was 3.5%. This rate is called the U3 rate and is the number of people without jobs and who have actively looked for work in the last four weeks.

But there’s a much more important rate that is rarely reported. The U6 unemployment really tells the full picture. It’s the U3 plus people who have stopped looking for work, plus part-time workers who want full time but can’t find any.

In September the U6 rate was 6.4%. Not quite as rosy as you’ve been led to believe, right?

Labor Participation

In addition to unemployment data, the BLS also tracks the percentage of the civilian population that is employed. This is the Labor Participation Rate.

In 2008 this rate was over 66%, but since then it had been declining until Covid hit at which time it cratered. As of September, 2022 the rate stood at 62.3%.

Each tenth of a percentage point represents about 160,000 workers. This means that when the percentage drops, a lot of people are not working and not paying Federal or Social Security taxes. Also they’re probably collecting unemployment payments. This situation exasperates the Federal deficit. In addition to a boost to individuals’ self-esteem, getting people back to work has many benefits to the Federal budget.

Inflation

I’ve written a lot previously about inflation. It affects every one of us. Gas prices, food prices, our electric bills – everything is going up at a crazy rate. Yes, I’m happy that my Social Security is going up 8.7% next year, but that increase probably only covers the extra I’m paying every month for gasoline and electricity.

How do we fix inflation? According to the noted economist Milton Friedman: “The only cure for inflation is to reduce the rate at which total spending is growing. There is no way of slowing down inflation that will not involve an… increase in unemployment, and a… reduction in the rate of growth of output.”

Quite simply, the fix for inflation is PAIN. It will take courage from our leaders to defeat inflation. Unfortunately, I don’t see that courage appearing anytime soon.

Interest Rates and Government Borrowing

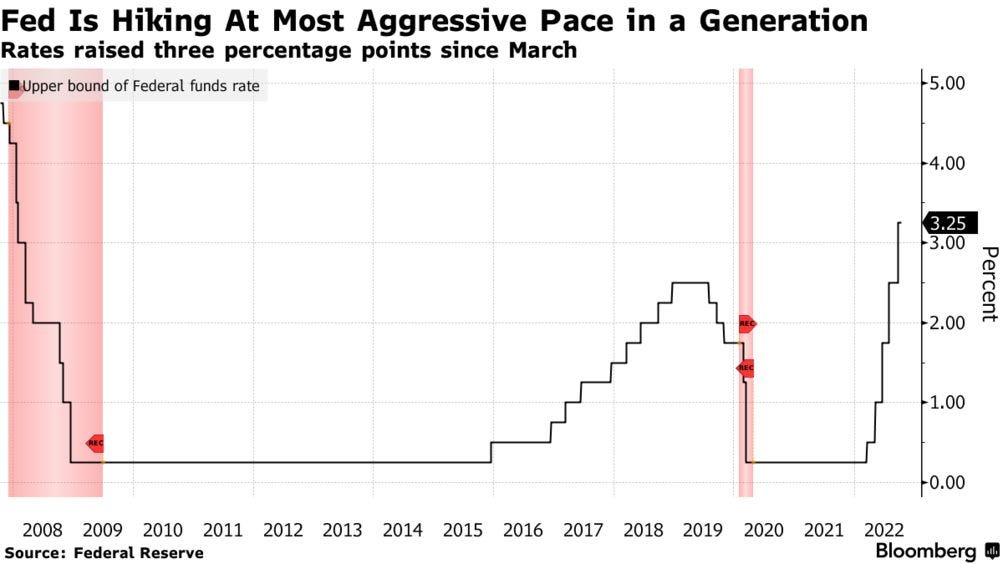

The Federal Reserve raises interest rates in order to slow down inflation. Unfortunately, when interest rates rise, borrowing costs for businesses and consumers increase. This has a dampening effect on our economy and can induce a recession.

In addition, government borrowing costs increase when rates rise. Our $31 trillion Federal debt costs an extra $310 billion with every 1% rise in interest rates.

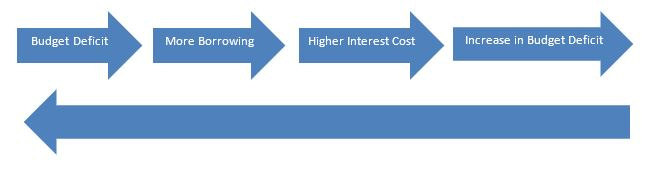

Rates and government borrowing go hand in hand when spending causes a budget deficit which, in turn, causes more government borrowing. And then when the Federal Reserve raises interest rates, the cost of government borrowing goes up, causing a larger deficit.

We could be in what Larry Summers refers to as a debit doom loop. It looks something like this:

Unfortunately, interest rates aren’t going to be headed down for a while. In fact some experts think The Fed may raise rates to 5.75% to purge inflation.

* * *

So, what do we do? That’s a question that I don’t have an easy answer for. Pay attention to your investments and try to avoid risky ones since those companies could be the first to go bankrupt. In an inflationary market, debt is your friend so be careful about prepaying mortgages and car loans. Try not to keep too much cash, as over time cash becomes less valuable with inflation.

If you’re still uncomfortable, talk to your financial advisor or accountant. They’ll know your personal situation and do a better job than I could here.

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

“When people are presented with the alternatives of hating themselves for their failures or hating others for their success, they seldom choose to hate themselves.”

- Thomas Sowell

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

Baby Goats Are So CUTE!

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~