What, Me Worry?

What, Me Worry?

A Different Way to Look at Your Investments

Your portfolio is like a bar of soap. The more you handle it, the smaller it gets.

- Unknown Investment Advisor

[This is my follow up to last week’s article where I promised to tell you about a different strategy for investing. I hope it’s helpful and thought provoking.]

Today I’m writing about a different way to look at investing. Note that I’m assuming that the majority of my readers are not sophisticated investors and are retired, so that’s the view I’m taking in this article. The same methods and objectives described here apply whether the investments are in a retirement or regular investment account. Also, I’d like to take a moment to remind you that I’m not advising you to make any particular investment. My writing here is purely educational.

But before we look at this different approach, let’s look at how your investments are probably structured today.

If your retirement was in a 401K or if you’re working with an advisor, almost certainly the funds are placed in one or more mutual funds. Mutual funds are run by professional managers who take your money, and that of thousands of others, and invest it in stocks and/or government and corporate bonds. The managers try to grow the money on your behalf and they charge a fee to do this. Mutual funds are legitimate investments and for the individual who wishes to take a passive approach to investing, either due to fear of making mistakes, unfamiliarity of investments or the desire to let someone else do the work, mutual funds have a place in investment accounts. Here’s a short video that explains some of the mutual fund basics:

Mutual funds have risks and troubles too. They have many questions that cannot always be readily answered:

Who’s the manager? What’s their track record? What’s their tolerance for risk?

What companies (or bonds) are in the fund? How risky are these investments?

What’s the income I will receive?

How much does the manager charge for fees? Is that higher or lower than the industry?

Most importantly, retirement distributions from mutual funds most often means selling mutual fund shares to raise cash to distribute. It is the sale of shares at a lower value in a down market that scares most people. When you’re withdrawing $1,000 per month and your portfolio’s value is $300,000 your money will last a lot longer than if your portfolio drops in value to $200,000.

* * *

So, what if I told you there’s a way to invest where the value of the portfolio doesn’t matter? A way where you’re investing in top-notch companies? A way that your income can grow organically year-to-year?

There is, and it’s not snake oil. It’s called “Dividend Growth Investing” or DGI.

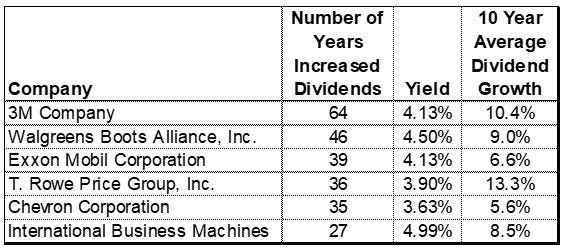

The principal of DGI is that you buy stock in individual dividend paying companies and not in mutual funds. And not just any company, but solid companies that increase their dividends each year. Need examples? Here are a few (as of 4/30/2022):

I’m sure you’ve heard of each of these companies. Imagine having bought 3M at some point in the past. It’s increased its dividend every year for 64 years! And over the last 10 years the increase has been averaging 10.4% per year. When was the last time YOU got a 10% raise? Oh, and BTW, 3M’s 4.13% yield is pretty darned good.

Believe it or not, there are over 140 NYSE or NASDAQ companies that have increased their dividends each year for 25 or more years. And there are hundreds more that have increased dividends for 10-25 years.

Ok you ask, this is nice, but how do I sleep well at night (SWAN) investing like this?

The secret is paying attention to the dividends and not the value of the stock. As an example, if you bought 3M company last fall and paid $180 per share for 100 shares, you received $1.49 per share per quarter in income, or $149 per quarter for about a 3.3% yield. Today (5/18/22) 3M is trading at about $150 per share, or a drop of about 16%. But you’re still receiving $149 a quarter in dividends. Yes, if you sold your stock today, you’d lose $30 per share. But, unless you think that 3M’s business is about to implode and they’re going to go bankrupt or cut their dividend, there is no reason to sell the stock. And, next year the $1.49 dividend will almost certainly increase.

Focus on the dividend, not the stock’s value.

If you structure your portfolio correctly, you can live off of dividends without selling any stock.

For example, consider Suzie. She has about $300,000 in her retirement account. She needs about $1,000 per month to supplement her social security. Suzie invests in the five companies mentioned earlier:

Suzie’s investment will return enough for her needs and, given the propensity of these companies to raise their dividends, she’ll have an increase in her income next year. But, the big takeaway from this example is that if the market drops 25% (and if the world doesn’t come to an end), Suzie’s $1,000 per month will not change.

Keep in mind that if I were Suzie I’d be investing in many more than five companies in order to diversify my portfolio and spread risk over many different investments.

* * *

I’m sure one of my readers will say “Ok, sure this sounds great, but some mutual funds have had long term growth rates of 10% or more. How does this compare?”

To that I’d say that there are over 7,500 mutual funds. Some of them may do very well, others perhaps not so much. Imagine sorting through these thousands of possible investments to find the best! Personally, I’d rather invest in Proctor & Gamble (66 years of dividend growth) or Johnson & Johnson (60 years of dividend growth). I can read about each of these companies and learn about them. I have their products in my home and I feel positive about them. Plus, I don’t have the time or energy to look through thousands of possible mutual fund investments. I’d have to do a lot more research with a typical mutual fund in order to answer some of the questions posed at the top of this article.

* * *

I hope you enjoyed this information. If you’d like to get a list of the Dividend Champions, you can request a copy here: https://secure.widemoatresearch.com/dividend-champions/. There’s a lot of information in the list but I’ll be happy to help you interpret it. Just email me at chuck.hardy@proton.me for help.

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

"Freedom is the right to tell people what they do not want to hear." - George Orwell

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

You Had One Job!

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~