All That Glitters

You’ve probably seen it in TV commercials: buy gold! Put gold in your IRA! Protect yourself from inflation, buy gold! So, I’m going to make a financial investment based upon what a second-rate actor says on TV? Not!

But it does beg the question: should I buy gold? And the companion question: should I buy silver?

The easy answer is “maybe.”

Maybe you’ve been contemplating buying gold. If you pay attention to the markets then you know that gold has just reached its all time high. If you’re looking to make a killing and if you’re a typical small investor and you buy high and sell low (tongue in cheek), then this is the time to buy!

Truly though there are many pundits who think gold could go higher in 2024. Will it? Dunno.

But I’m getting ahead of myself. The first question you need to ask yourself is why do you want to buy gold?

*** Note: everything I’m writing about gold also applies to silver. The numeric examples below are for gold but I believe silver’s numbers would be similar.

As an Investment?

Gold is probably a bad investment on its own. As they say, gold “has never been worth zero.” But its value could approach zero.

That said, gold could lose significant value. But gold still has military, industrial and technology value. For example, an average cell phone has about 30 milligrams (or about $0.05) of gold. For this reason alone, gold’s value will never go to zero.

In that respect I will say that gold is better than cryptocurrency like Bitcoin which I feel is the Kardashian of investments: it’s valuable for being valuable. There’s nothing securitizing Bitcoin, nor is there a common use for Bitcoin.

Another reason gold is probably a bad investment is that it does not generate income which can be important if you’re retired. Stocks usually pay dividends; bonds pay interest. Even your common savings account pays something. Gold pays you nothing.

So, as an investment, gold has two significant risks: 1) risk of loss of value; and, 2) risk of loss of income.

For those reasons, I think gold is lousy as an investment.

*** Important note: I see ads for the gold companies telling people that they can move their IRAs into gold and silver. I truly believe that is a MAJOR mistake for the risks and reasons above.

As an Inflation Hedge?

This is a bit more realistic.

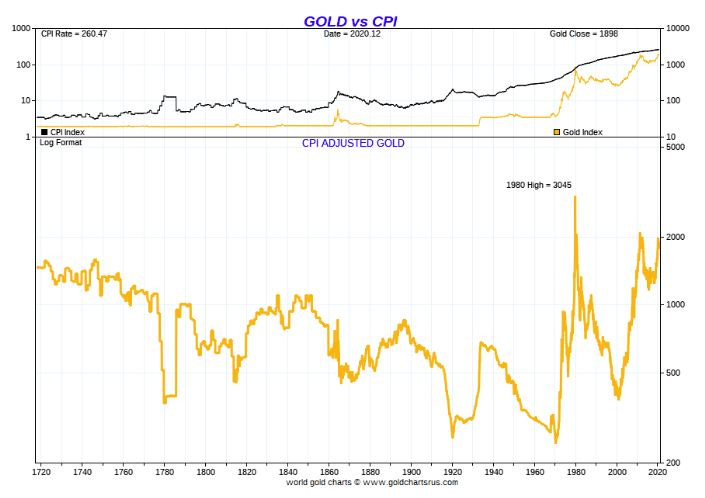

Here’s an interesting chart. It’s The value of an ounce of gold, adjusted by the Consumer Price Index, from 1700 to December 2020.

What I find very interesting is that if you had purchased an ounce of gold in 1700, it would have cost about $1,600 in today’s dollars. Considering that gold today (as I write this) is $2,080, over 320 years (1700 – 2020), the annual rate of return is 0.0082%. That’s pretty close to zero and, as a rate of return, is pretty terrible (another reason gold is a lousy investment).

But, if your goal was to preserve the value of your money, it’s pretty good. How do I know this? Well, if you had a $10 bill (were there was such a thing in 1700) you would still have $10 today. That $10 in 1700 would be worth about $772 in purchasing power today. Inflation cost you 99.87% of your money! With gold, the ounce of gold you bought in 1700 for $1,600 would be worth $2,080 today. Not bad!

Keep in mind though that if you bought gold in 1980, you paid about $3,000 in today’s dollars. Not good!

So, gold is a pretty good inflation hedge, but only if you are smart about when you buy it.

If You’re a Doomsday Prepper?

Here’s where gold shines (pun intended). Everyone knows gold. Gold can be a universally-accepted medium of exchange. The same applies to silver.

Are you thinking the fit might hit the shan? Well, based upon comments I received from my October article Could It Be The End? a lot of you are thinking about this possibility. I don’t necessarily mean Armageddon, but think about an economic depression like 1929. It could happen.

Imagine having a few hundred silver U.S. dimes minted before 1965. Right now, each one is worth $1.75 for its silver. If you needed to barter, you could buy a loaf of white bread for one silver dime.

A silver quarter of the same vintage is worth $4.38. That’ll buy a gallon of gasoline.

Similarly, a $5 U.S. gold piece is worth about $525 today. Each one contains about ¼ ounce of gold.

If you’re stockpiling gold and silver for the apocalypse, you can’t do worse than buying gold and silver U.S. coins. Not the fancy collector coins, but the “junk” coins – coins that collectors have no interest in.

Here are a couple of examples. Both are from the store Apmex.com which I am not endorsing but, full disclosure, I have purchased from in the past because of their excellent prices and service.

Notice that the $5 coin is noted as “cleaned”, meaning that someone defaced it by trying to make it look nicer. Anathema to a collector! But perfect for the bullion investor as there is no collector value assigned to the coin. Similarly, the Roosevelt dimes are “average circulated”, meaning that these were carried around in someone’s pocket or purse and show wear. No collector wants these.

So, why coins? Well, imagine buying a one-ounce gold bar for $2,100. Or a 10-ounce silver bar for $275. How do you make change for these? How do you buy $50 in gasoline with a 10-ounce silver bar? Gold and silver coins can offer smaller values with more legitimacy.

U.S. coins are readily identifiable and are difficult to counterfeit. That one-ounce gold bar might look suspicious to another person. But everyone knows the Roosevelt dime.

Verdict: gold and silver U.S. coins (versus gold and silver bars) are good mediums of exchange when there is a barter system. And, as gold and silver they offer investment and inflation protection.

* * *

So, should you buy gold? My thought is yes. I believe that every portfolio should have some amount, perhaps five or ten percent, in physical gold and silver.

Also, if you do buy physical gold, take possession of it. Many of the gold sellers will hold the gold for you. That’s not cool if the company goes bankrupt or there’s a financial meltdown. If you have that much gold, spend a few dollars and buy a safe.

Whether you decide to buy gold and silver is (obviously) up to you. If you do, do your own research and go into it with your eyes open and understand the risks.

Good luck!