Have you ever had a time in your life where your income didn’t exceed your expenses? A time when your hours at work were cut, or the company stopped paying overtime? Maybe you or your spouse lost their job and your income was cut in half.

I have.

How do you survive? Long term you need to make major changes to your finances. Sell stuff. Trade that luxury car in on a used Hyundai. Maybe move.

But short term? After you exhaust your savings, what do you do? You max out your credit cards. Maybe you even apply for a couple more while you can. You put your groceries on credit cards. You take cash advances from credit cards to make payments on other credit cards.

Short term this might work if you can get back on your feet quickly but if you don’t? Bankruptcy? How do you recover from this otherwise?

Well, the United States has been charging its groceries on credit cards and our country is nearing the point where our credit cards are maxed out.

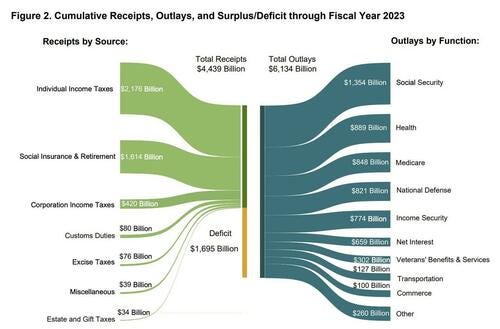

So, in 2023 the U.S. took in $4,439 billion in taxes and spent $6,134.

This is like someone earning $72,500 a year but spending $100,000 and putting $27,500 on credit cards each year.

According to CNBC, the U.S. national debt is rising by $1 trillion about every 100 days.

Recently, Moody’s Investors Service lowered its ratings outlook on the U.S. government to “negative” from “stable” due to the rising risks of the country’s fiscal strength.

“In the context of higher interest rates, without effective fiscal policy measures to reduce government spending or increase revenues,” the agency said. “Moody’s expects that the U.S.’ fiscal deficits will remain very large, significantly weakening debt affordability.”

Recent Treasury data show that budget deficit grew 16 percent from a year ago, pushing the federal budget shortfall to $532 billion in the first four months of this fiscal year.

Business leaders are starting to sound the alarm:

Fred Smith, the founder of FedEx, is the latest business leader to sound the alarm that if America’s ballooning public debt is left unchecked, it will threaten to spiral into a catastrophic crisis.

JPMorgan Chase CEO Jamie Dimon warned that out-of-control spending in Washington threatens a government default that could trigger a “rebellion.”

Billionaire investor Ken Griffin said that trying to print more dollars to deal with the possibility of a default would push the economy into a “deep tailspin.”

Academics are worried:

According to E.J. Antoni, Economist for the Heritage Foundation: “CBO estimates interest on federal debt as a percent of GDP will set a new record by next year”

Analysts at the University of Pennsylvania estimate that when the debt-to-GDP ratio hits around 200 percent, it will hit the point of no return. That’s when no amount of future tax increases or spending cuts could prevent the government from defaulting on its debt.

So, everyone is worried about the budget deficit, except for Congress. In the $460 billion spending bill just passed to prevent the impending (oh, the humanity!) government shutdown, here are some earmarks that, apparently, the United States of America just can’t do without:

The Waadookodaading Ojibew Language Institute in Wisconsin will get $5 million

$1.65 million to build an “artists' living and workspace” with the Environmental Leaders of Color in New York

$1 million for sugarcane research in Louisiana

$1 million will go to 'electric vehicle infrastructure 'masterplan' in Chicago

Providence, Rhode Island will get $1 million for a 'city-wide climate assessment'

Florida will get $190,000 for a 'shark repellent study' in Sarasota

Juvenile Pacific Salmon Research in Alaska will get $4 million

Public housing residents in California will get $1 million for an electric vehicle car share

As they say, all this and more!

* * *

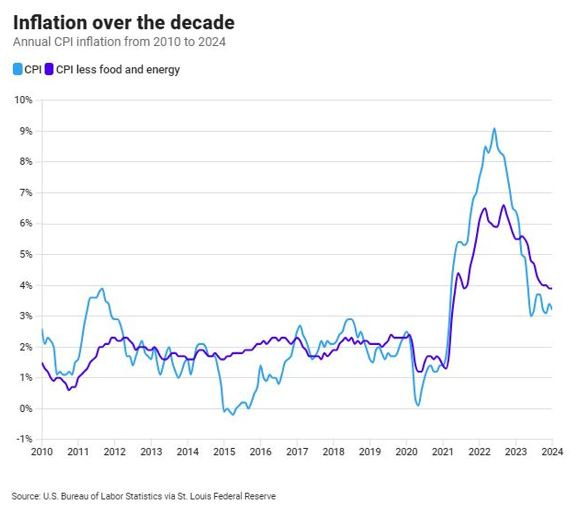

The “sugar rush” in the economy from Covid spending has caused inflation and interest rates to rise to levels not seen in years.

What does this mean? Well, there are a number of problems that can, and most likely will, occur with this much debt and government spending:

Fresh out of Covid relief money, the U.S. consumer has curtailed spending with retail sales dropping 0.8% in January, much more than expected, per CNBC.

Inflation continues apace. In January consumer prices increased 0.3%, but car insurance premiums jumped 1.4%.

Some experts are forecasting a depression in commercial real estate due to high interest rates. In fact, recently a Canadian pension fund sold its 29% interest in a Manhattan office tower for $1. This transaction has shaken the commercial real estate marketplace. Community banks that hold much commercial real estate loans are under pressure and we may see more failures in the next 1-2 years.

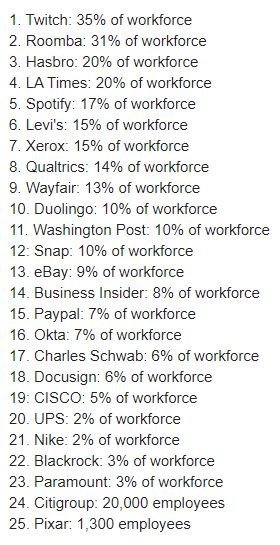

There have been numerous mass layoffs amounting to tens of thousands of workers. See below for a partial list.1

* * *

So, what happens?

When we contemplate the U.S. fiscal predicament, keep in mind that there are only four means by which government can capture resources for its own use:

Outright confiscation of property for public use, which is prevented by the U.S. Constitution’s “taking clause” without just compensation of the property owner.

Taxation.

Debt issuance.

Inflation that erodes the nominal amount of the debt over time, harming lenders.

Some observers would argue that this fourth strategy is perhaps what we are beginning to observe in the U.S. and some other countries around the world.

Of course, the U.S. must cut spending to facilitate paying off the debt. This could lead to civil conflict as somebody’s ox will be gored.

What do you and I do about it?

Unfortunately, not much.

Without sounding like a broken record, you can put some of your assets in “hard” investments like physical silver and gold bullion.

If the government is going to use inflation to make it easier pay off the debt, you want to decrease the amounts you keep in bank CDs and savings accounts and reduce your holdings in corporate, municipal and U.S. Treasury bonds. This is because inflation will decrease the purchasing power of those dollars.

Don’t make early payments to any loans you have. You’ll make future payments with cheaper, inflated dollars.

Batten down the hatches, the ride is going to be bumpy.

Major layoffs in 2023:

Been there, but changed my life style At once and never let my spending exceed my income, eventually everything worked out and no longer have to worry